Airports are a critical component of the US multimodal transportation system because they efficiently and safely facilitate the movement of people, goods, and services. This role was highlighted in MAP-21 with the inclusion of “aerotropolis transportation systems” as strategic destinations for state resources intended to improve the overall performance of the transportation system. Airports not only enable economic activity—they generate economic activity as places of employment, purchasers of goods and services, and attractions for travelers.

Two recent economic impact reports highlight aviation’s important role as a source of economic activity. The FAA released The Economic Impact of Civil Aviation on the U.S. Economy in August 2011. This report states that the civil aviation industry contributed approximately 10.2 million jobs, $394.4 billion in earnings, and $1.3 trillion in annual output to the US economy in 2011 (approximately 5.2 percent of total gross domestic product). The study provided a breakdown for different portions of the civil aviation industry including airline operations, airport operations, various associated manufacturing segments, other related service providers, contributions from the general aviation community, and FAA spending.

In January 2012, CDM Smith released, The Economic Impact of Commercial Airports in 2010, an economic impact study that used a different methodology but reported similar findings: 10.5 million jobs, annual payrolls of roughly $365 billion, and $1.2 trillion in annual output. This study focused on 490 US commercial airports, and measured their direct, multiplier, and total impacts in terms of employment, payroll, and output at the state level. This report found the 80 commercial airports in the MAFC region were responsible for almost 1.5 million jobs, contributed almost $55 billion to annual payrolls, and created just over $10 billion in economic output.

Table 1: Airports, Jobs, Payroll, and Economic Output in the MAFC

| Region | Number of Airports | Jobs | Payroll | Output |

| Illinois | 10 | 454,280 | $18,282,773,000 | $50,673,207,000 |

| Indiana | 5 | 83,150 | $2,322,530,000 | $8,858,534,000 |

| Iowa | 8 | 16,880 | $598,205,000 | $1,824,820,000 |

| Kansas | 7 | 39,750 | $2,152,634,000 | $8,846,916,000 |

| Kentucky | 4 | 136,370 | $3,713,041,000 | $14,038,514,000 |

| Michigan | 16 | 179,290 | $6,533,485,000 | $18,608,708,000 |

| Minnesota | 9 | 148,610 | $6,310,044,000 | $24,913,504,000 |

| Missouri | 6 | 178,540 | $5,776,404,000 | $18,685,053,000 |

| Ohio | 7 | 136,500 | $4,658,754,000 | $13,608,778,000 |

| Wisconsin | 8 | 105,430 | $3,313,530,000 | $10,215,395,000 |

| MAFC | 80 | 1,478,800 | $53,661,400,000 | $170,273,429,000 |

| US | 490 | 10,497,430 | $365,329,988,000 | $1,178,946,616,000 |

Source: The Economic Impact of Commercial Airports in 2010

Airports offering air cargo facilities provide a shipping option that can spur economic development in two ways. First, it can open new markets for locally produced goods. Second, it can induce activity in specific industries (both goods producing and service providing industries such as warehouses, freight forwarders, and other logistic companies) in order to take advantage of the opportunities air transportation provides to supply chains. Both types of activity affect production, earnings, and employment levels locally and in the surrounding region.

Air cargo’s total contribution to the economy, as figured in 2008 by the FAA, amounts to roughly $1.6 trillion in output, $436.4 billion in earnings, and 9.3 million jobs. For more information about individual airport and statewide aviation economic impact studies, and other economic impact, download the Economic Impacts of Air Cargo in the MAFC spreadsheet.

Table 2: Economic Impact of Air Cargo in 2008

| Freight Exports | Domestic Freight | Total Freight | |

| Output | |||

| Value of Air Freight ($Billions) | 387.3 | 174.8 | 562.1 |

| Total Output ($Billions) | 1,137.6 | 511.0 | 1,648.6 |

| Earnings | |||

| Indirect Earnings ($Billions) | 102.4 | 46.4 | 148.7 |

| Total Earnings ($Billions) | 300.8 | 135.6 | 436.4 |

| Employment | |||

| Indirect Employment (Millions) | 2.2 | 1.0 | 3.2 |

| Total Employment (Millions) | 6.4 | 2.9 | 9.3 |

Source: The Economic Impact of Civil Aviation on the U.S. Economy

Goods shipped via air are normally considered to be high in value. Shipping by air provides reliable deliveries with fast transit times, and therefore commands high prices to do so. In certain parts of the country, shipping goods via air transportation is the only option for delivering goods. Generally speaking, shippers who produce the following products are most likely to utilize air transit to ship their goods: pharmaceuticals and other chemicals, machinery, transportation equipment, medical equipment and other precision instruments, computers and electronics, perishable goods such as flowers, and mixed freight.

Table 3: Value of Commodities Transported by Air in 2008

| Commodity | Domestic and Export Flows ($Billions) |

| Electronics | 201.9 |

| Machinery | 101.8 |

| Precision Instruments | 83.0 |

| Misc. Manufacturing Products | 40.7 |

| Transport Equipment | 37.2 |

| Pharmaceuticals | 30.1 |

| Basic Chemicals | 10.7 |

| Chemical Products | 10.7 |

| Articles-Base Metal | 10.7 |

| Plastics/Rubber | 6.3 |

| All Commodities | 562.1 |

Source: The Economic Impact of Civil Aviation on the U.S. Economy

In additional to the Top 5 commodities via air cargo for each MAFC state, you can also download the commodity totals (kilotons, ton miles, and value in millions of dollars) exported and imported for each MAFC state transported by air cargo:

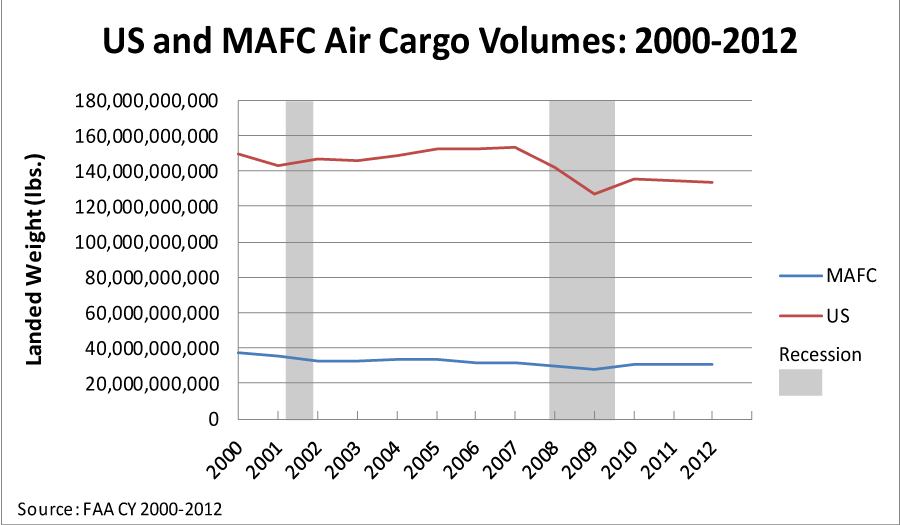

Air cargo volumes for the United States and the MAFC are both recovering from the 2009 lows reached during the Great Recession, but neither have reached the levels at the turn of the century. The MAFC’s share of US air cargo volume since 2000 ranged from a high of 25.11 percent in 2000 to a low of 20.47 percent in 2007, while its share in 2012 accounted for 23.44 percent of the national total.

Figure 1: US and MAFC Air Cargo Volumes

The data used to render Figure 1 is also available for download as Landed Weights in the MAFC.

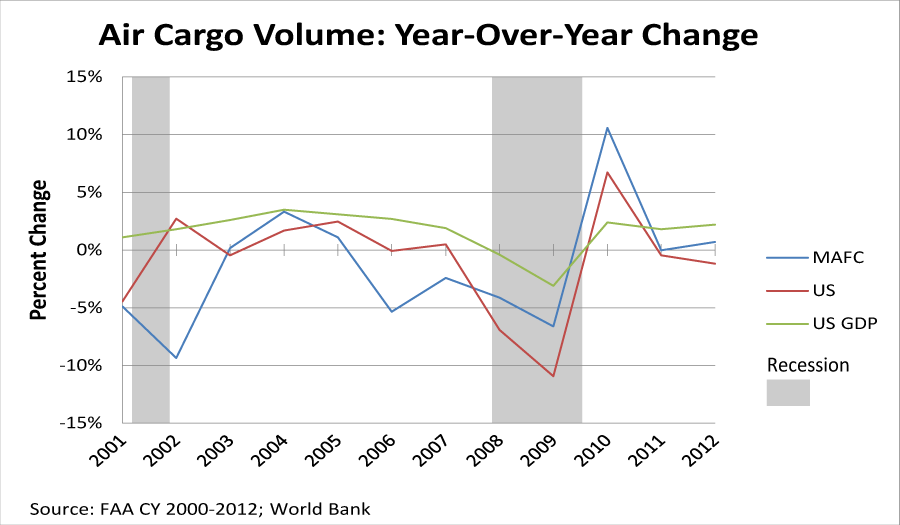

Figure 2: Air Cargo Volume: Year-over-Year Change

The data used to render Figure 2 is also available for download as Year-over-Year Landed Weight Changes in the MAFC.

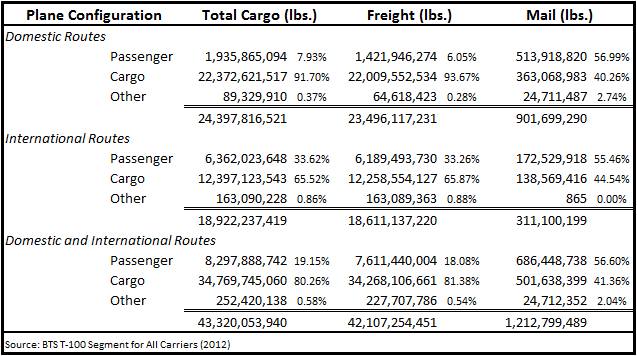

Analysis of 2012 BTS T-100 data shows roughly 80 percent of total air cargo (freight and mail) that travels to, from, or within the United States does so on planes with a cargo configuration, while just over 19 percent of total air cargo travels in passenger planes. There is a distinct difference however, when comparing domestic routes (approximately eight percent in passenger planes compared to almost 92 percent in cargo planes) to international routes (just under 34 percent in passenger planes versus about 65 percent).

Table 4: Plane Configuration Market

Passenger enplanements for the 27 air cargo airports within the MAFC regional was just under 100 million in 2012, which was down from the peak in 2005 at just under 120 million. The MAFC air cargo airports market share of the total US passenger enplanements has trended lower since 2002 from 17.32 percent to 13.63 percent in 2012.

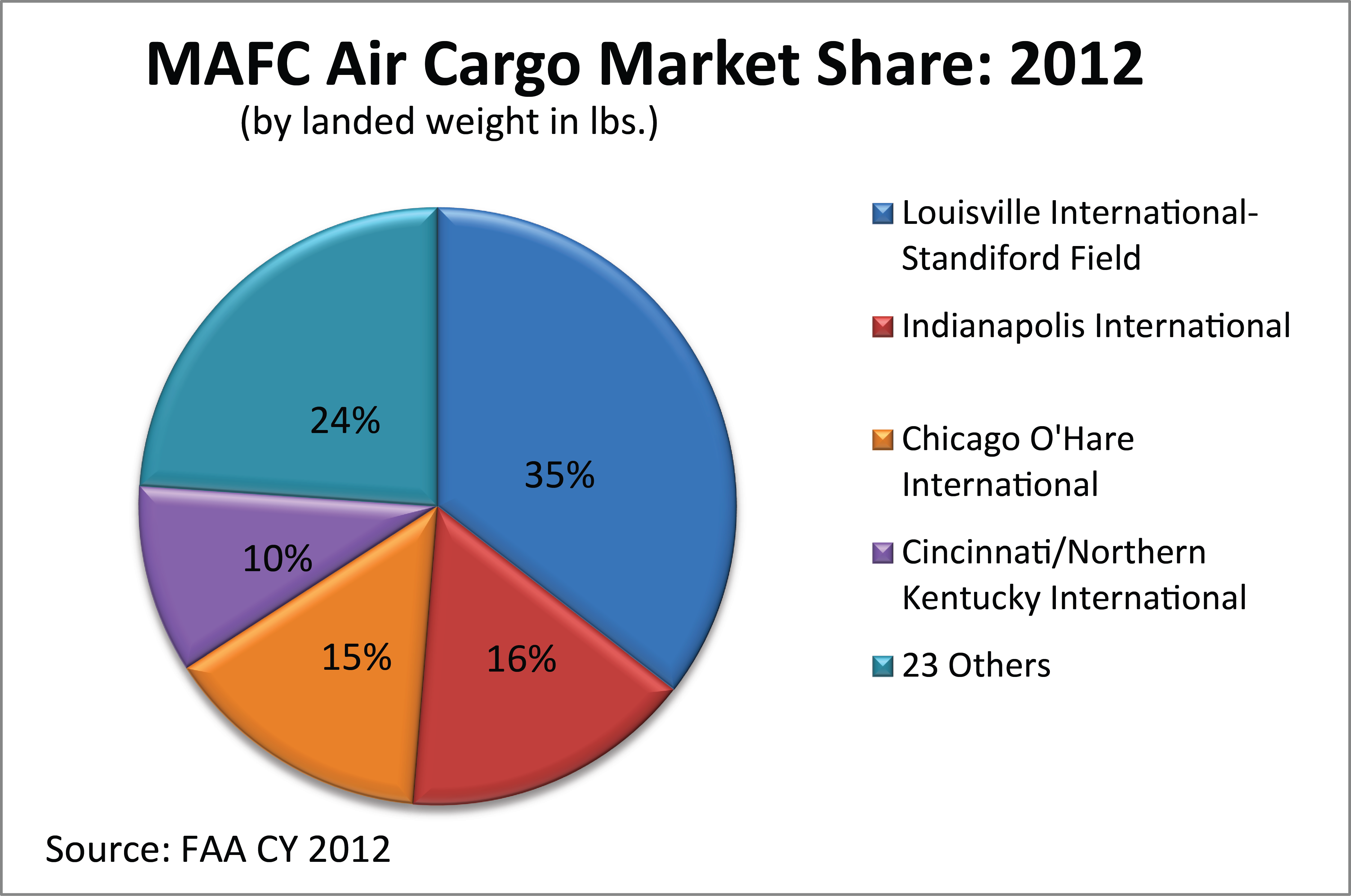

While the Federal Aviation Administration (FAA) reported air cargo data for 27 airports within the MAFC and its associated metropolitan statistical areas in 2012, four airports dominated market share (by landed weight in pounds). Louisville International – Standiford Field, which is home to UPS Worldport and ranked third overall in the nation, accounted for 35.5 percent of air cargo by landed weight. Indianapolis International, Chicago O’Hare International, and Cincinnati/Northern Kentucky International with 15.8, 14.6, and 10.2 percent, respectively, make up a second tier of air cargo ports and rank 5th, 6th, and 9th nationally. The remaining 23 airports accounted for roughly 24 percent of the MAFC’s landed air cargo weight.

Figure 3: 2012 Air Cargo Market Share in the MAFC

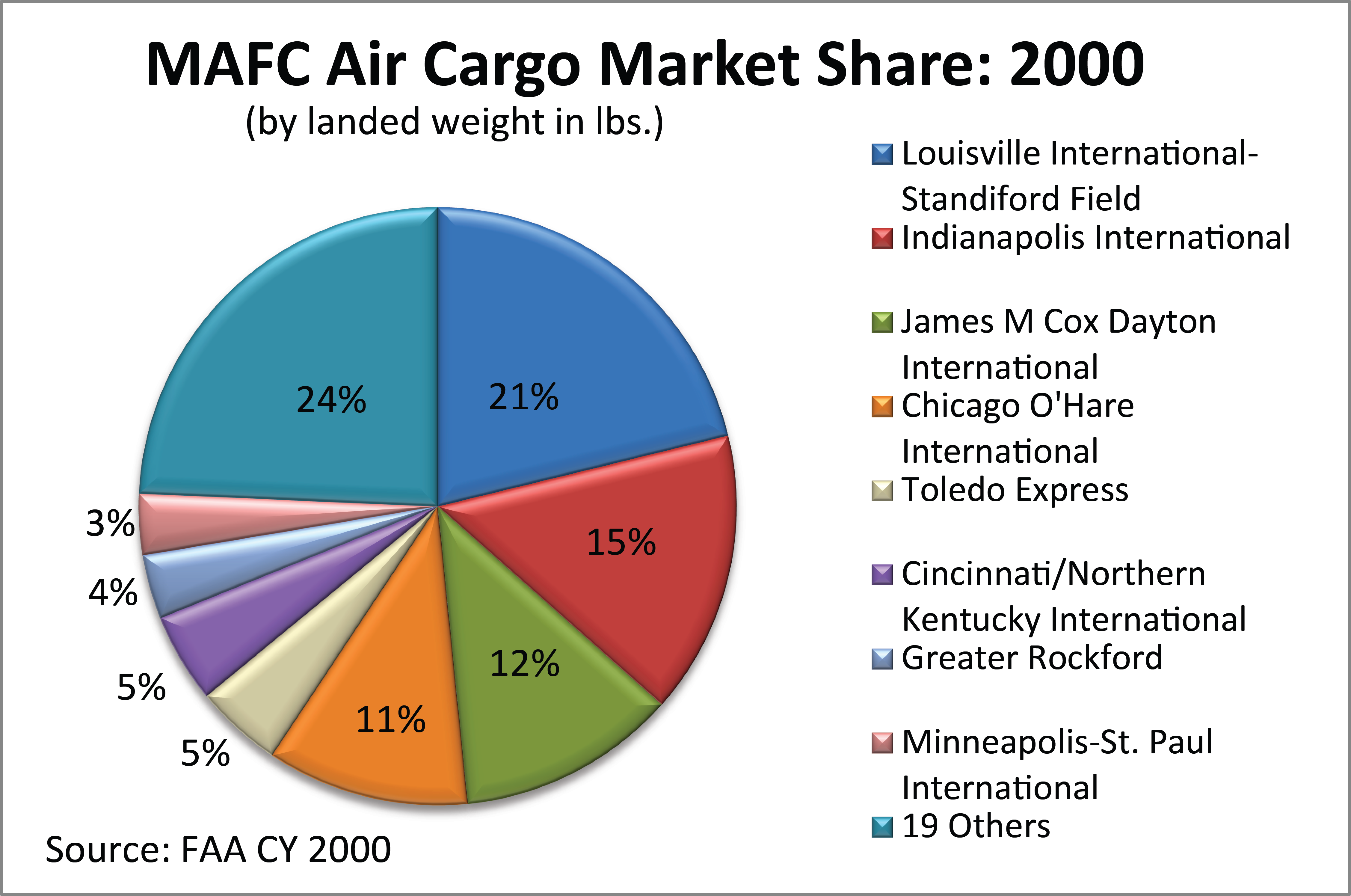

Market share in the MAFC looked significantly different in 2000. While in 2012 four airports accounted for roughly three-fourths of the total landed weight, in 2000 eight airports were needed to reach the same percentage of market share. Louisville International – Standiford Field’s market share has increased significantly from its 21 percent in 2000. While Indianapolis’ market share has not changed much, Cincinnati/Northern Kentucky International’s market share has doubled, Chicago O’Hare International’s has increased from 11 to 15 percent, and airports such as James M. Cox Dayton International and Toledo Express have seen drastic reductions in air cargo volumes.

Figure 4: 2000 Air Cargo Market Share in the MAFC

Individual airport BTS statistics regarding scheduled departures, scheduled carriers, top destinations, freight/mail (pounds), and on-time performance are available as individual spreadsheets: